Ever heard someone mention the “Rule of 78” when talking about car loans? It sounds a bit like something out of a dusty old textbook‚ doesn’t it? Well‚ you’re not wrong! This method of calculating interest on loans‚ particularly when paying them off early‚ was once quite common. But is it still relevant today? Let’s dive in and explore what the Rule of 78 is‚ why it was used‚ and whether you need to worry about it when financing your next car. We’ll break down the complexities and see if this relic of the past still holds any sway in the modern world of auto loans.

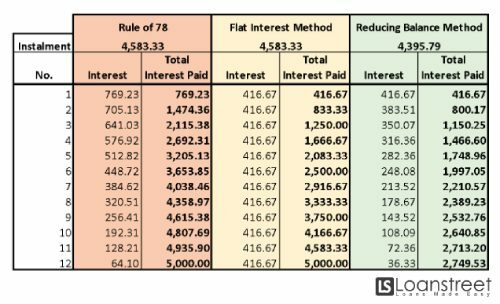

The Rule of 78‚ also known as the “sum of the digits” method‚ is a way to front-load interest on a loan. This means that in the early months of the loan‚ a larger portion of your payment goes towards interest‚ and a smaller portion goes towards the principal. As the loan progresses‚ this ratio gradually shifts. Why was this done? Primarily‚ it benefited lenders‚ especially if borrowers paid off their loans early.

Here’s the basic idea:

For a 12-month loan‚ you add up the numbers 1 through 12 (1+2+3…+12 = 78). Hence‚ the name “Rule of 78.”

In the first month‚ 12/78 of the total interest is charged.

In the second month‚ 11/78 of the total interest is charged‚ and so on.

So‚ if you were to pay off the loan early‚ the lender would keep a larger chunk of the interest than if the interest was calculated evenly over the loan term. Sneaky‚ right?

Interesting Tip: The Rule of 78 was more prevalent in the past when loan calculations were done manually. It provided a relatively simple way to allocate interest compared to more complex amortization schedules.

Thankfully‚ the Rule of 78 is becoming increasingly rare in the world of car loans. There are several reasons for this decline. For starters‚ consumer protection laws have become more robust‚ aiming to prevent lenders from taking advantage of borrowers. Modern technology also plays a role. With sophisticated computer systems‚ lenders can easily calculate interest using more accurate and transparent methods‚ like simple interest.

Here are some key factors contributing to its decline:

Consumer Protection Laws: Regulations are in place to ensure fair lending practices.

Technological Advancements: Computers make it easy to use more precise interest calculation methods.

Increased Transparency: Borrowers demand clear and understandable loan terms.

Essentially‚ the Rule of 78 is seen as outdated and potentially unfair in today’s lending environment. Lenders are now more likely to use simple interest‚ where interest is calculated based on the outstanding principal balance.

Simple Interest vs. Car Loans Rule of 78

What’s the difference? With simple interest‚ you only pay interest on the amount of principal you haven’t yet paid off. This means that if you make extra payments‚ more of your money goes directly towards reducing the principal‚ saving you money on interest in the long run. The Rule of 78‚ on the other hand‚ doesn’t offer this advantage to the same extent.

Information Callout: Always ask your lender how interest is calculated on your car loan. If they mention the Rule of 78‚ consider exploring other financing options.

How to Protect Yourself from Car Loans Rule of 78

Even though the Rule of 78 is less common‚ it’s still wise to be vigilant. Here’s how you can protect yourself:

Read the Fine Print: Carefully review your loan agreement to understand how interest is calculated. Look for any mention of the Rule of 78 or “sum of the digits” method.

Ask Questions: Don’t hesitate to ask your lender to explain the interest calculation process in detail.

Compare Loan Offers: Shop around and compare loan offers from multiple lenders. Look for loans with simple interest.

Consider Prepayment Penalties: Check if there are any penalties for paying off your loan early. This can be a red flag if the lender is using a less favorable interest calculation method.

By being informed and proactive‚ you can ensure that you’re getting a fair deal on your car loan and avoid any unpleasant surprises down the road.

Understanding Loan Amortization Schedules

A loan amortization schedule is a table that shows how much of each payment goes towards principal and interest over the life of the loan. Requesting this schedule from your lender can give you a clear picture of how your loan is structured and help you identify any potential issues.

FAQ About Car Loans and the Rule of 78

Q: Is the Rule of 78 illegal?

A: No‚ the Rule of 78 isn’t inherently illegal in all jurisdictions‚ but its use is heavily regulated and restricted in many places due to concerns about fairness and transparency.

Q: How can I tell if my car loan uses the Rule of 78?

A: Check your loan agreement for any mention of the Rule of 78 or “sum of the digits” method. If the interest charges seem disproportionately high in the early months of the loan‚ it could be a sign that the Rule of 78 is being used.

Q: What should I do if I think my loan uses the Rule of 78 unfairly?

A: Contact your lender and express your concerns. If you’re not satisfied with their response‚ consider filing a complaint with a consumer protection agency or seeking legal advice.

Q: Are there any situations where the Rule of 78 might be beneficial?

A: Generally‚ the Rule of 78 is rarely beneficial for borrowers. It primarily benefits lenders‚ especially if the loan is paid off early.

So‚ while the Rule of 78 might be a fading memory in the car loan world‚ it’s still important to be aware of its existence. Always do your research‚ ask questions‚ and protect yourself from potentially unfair lending practices. By staying informed‚ you can drive away with confidence‚ knowing you’ve secured the best possible financing for your new ride. Remember‚ knowledge is power when it comes to navigating the complexities of car loans. Don’t be afraid to ask questions and advocate for yourself. A little bit of research can save you a lot of money and stress in the long run. Happy car shopping!

Emily combines her passion for finance with a degree in information systems. She writes about digital banking, blockchain innovations, and how technology is reshaping the world of finance.

Emily combines her passion for finance with a degree in information systems. She writes about digital banking, blockchain innovations, and how technology is reshaping the world of finance.